Two big banks have released long-term economic outlooks. This is what brokers need to know

The Canadian economy is performing stronger than it was during a difficult second quarter, according to the National Bank of Canada, but the Bank of Canada will likely hold its benchmark interest rate for the foreseeable future.

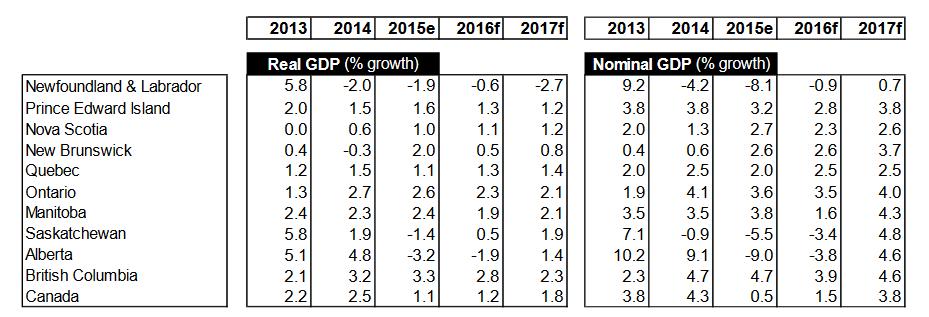

“We are keeping unchanged our Canadian GDP growth forecasts for both this year and next at 1.2% and 1.8% respectively. Unless the upcoming fiscal stimulus from the federal government is targeted effectively as to lift the economy’s potential, Canada will be stuck in low-growth mode,” National Bank’s economists said in their latest Economic Outlook. “Facing a lower real neutral interest rate, also a result of declining potential growth, the Bank of Canada will have no alternative other than keep the overnight rate low for years to come.”

On the positive side, exports saw an uptick in July and Canadian consumers are benefitting from the enhanced Canada Child Benefit, the authors said. “However, investment remains disappointing, hurting economic growth not just contemporaneously but also in the future via a lower potential.”

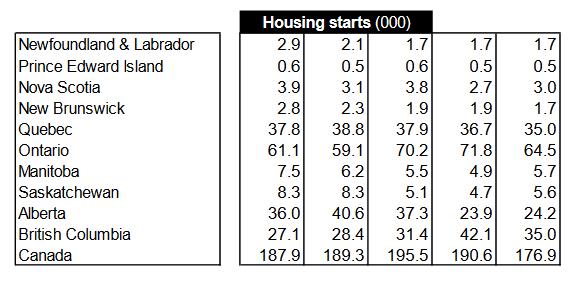

As for housing starts, the bank is forecasting slight softening across the country.

After averaging 190,800 starts a year since 2013 (including a forecasted 190,600 for 2016), National Bank is forecasting 176.900 starts in 2017.

Ontario is forecasted to have 64,500 starts next year (compared to 71,800 forecasted for 2016); British Columbia is expected to have 35,000 starts in 2017 (compared to a forecasted 42,100 this year).

However, Alberta is expected to see a slight uptick in starts. National Bank forecasts 24,200 in 2017, up from 2016’s expectation of 23,900.

For its part, TD Bank predicts the Bank of Canada will hold its target at 0.5% until sometime in 2019, when it is hiked to 1%. That will eventually give way to another interest

rate hike in 2020, according to TD, when it will settle in at 1.25% to close out the year.

“Slower trend economic growth will also restrain the level of interest rates. With excess capacity expected to be absorbed slowly over the next several years, the Bank of Canada is likely to leave rates at their current 1.00% level until early 2019,” TD said in its Long-term Economic forecast. “Even as rates move higher, they are likely to rise to just 1.25% by the end of the forecast horizon in 2020.”

Variable mortgage rates are closely tied to the overnight rate; fixed mortgage rates, on the other hand, are impacted by bond yields.

TD Predicts the five-year government bond yield will steadily increase starting next year. The five year yield closed out 2015 at 0.73% and it is expected to end 2016 at 0.7%.

However, it will eventually see slight upticks each year.

The bank forecasts the five-year bond yield percentage will be 0.95% at the end of 2017, 1.30% at the end of 2018, 1.55% in 2019, and 1.80% in 2020.

Rates are dependent on a number of economic factors. This year, the economy is expected to grow by a mere 1.1% this year. However, it is expected to grow to 1.8% next year, driven, in large part, by rebuilding efforts due to the Alberta wildfires this year.

See below for detailed provincial stats

Sources: CMHC, Statistics Canada, National Bank

“We are keeping unchanged our Canadian GDP growth forecasts for both this year and next at 1.2% and 1.8% respectively. Unless the upcoming fiscal stimulus from the federal government is targeted effectively as to lift the economy’s potential, Canada will be stuck in low-growth mode,” National Bank’s economists said in their latest Economic Outlook. “Facing a lower real neutral interest rate, also a result of declining potential growth, the Bank of Canada will have no alternative other than keep the overnight rate low for years to come.”

On the positive side, exports saw an uptick in July and Canadian consumers are benefitting from the enhanced Canada Child Benefit, the authors said. “However, investment remains disappointing, hurting economic growth not just contemporaneously but also in the future via a lower potential.”

As for housing starts, the bank is forecasting slight softening across the country.

After averaging 190,800 starts a year since 2013 (including a forecasted 190,600 for 2016), National Bank is forecasting 176.900 starts in 2017.

Ontario is forecasted to have 64,500 starts next year (compared to 71,800 forecasted for 2016); British Columbia is expected to have 35,000 starts in 2017 (compared to a forecasted 42,100 this year).

However, Alberta is expected to see a slight uptick in starts. National Bank forecasts 24,200 in 2017, up from 2016’s expectation of 23,900.

For its part, TD Bank predicts the Bank of Canada will hold its target at 0.5% until sometime in 2019, when it is hiked to 1%. That will eventually give way to another interest

rate hike in 2020, according to TD, when it will settle in at 1.25% to close out the year.

“Slower trend economic growth will also restrain the level of interest rates. With excess capacity expected to be absorbed slowly over the next several years, the Bank of Canada is likely to leave rates at their current 1.00% level until early 2019,” TD said in its Long-term Economic forecast. “Even as rates move higher, they are likely to rise to just 1.25% by the end of the forecast horizon in 2020.”

Variable mortgage rates are closely tied to the overnight rate; fixed mortgage rates, on the other hand, are impacted by bond yields.

TD Predicts the five-year government bond yield will steadily increase starting next year. The five year yield closed out 2015 at 0.73% and it is expected to end 2016 at 0.7%.

However, it will eventually see slight upticks each year.

The bank forecasts the five-year bond yield percentage will be 0.95% at the end of 2017, 1.30% at the end of 2018, 1.55% in 2019, and 1.80% in 2020.

Rates are dependent on a number of economic factors. This year, the economy is expected to grow by a mere 1.1% this year. However, it is expected to grow to 1.8% next year, driven, in large part, by rebuilding efforts due to the Alberta wildfires this year.

See below for detailed provincial stats

Sources: CMHC, Statistics Canada, National Bank