One broker said he is getting nowhere in trying to find out why TD has altered the fine print in its VRM contracts for conventional mortgages – specifically around when a spike in LTV triggers demand for a lump-sum payment or a new appraisal.

One broker said he is getting nowhere in trying to find out why TD has altered the fine print in its VRM contracts for conventional mortgages – specifically around when a spike in LTV triggers demand for a lump-sum payment or a new appraisal.

“I went to the BDM and I ran it past them and asked if I was reading it wrong or not understanding it properly and they said the intention is as it states,” Patrick Mulhern of Invis Mulhern Mortgages told MortgageBrokerNews.ca. “They didn’t explain why the change was made.”

He suspects that change is really a hedge against any future price correction for Canadian real estate.

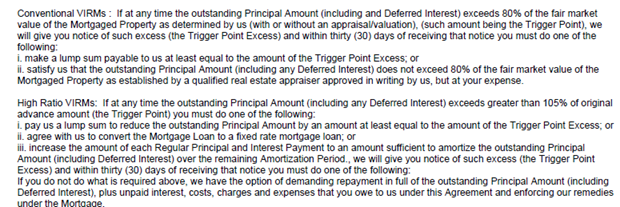

Under the terms of the new clause, if, at any time and for any reason, the loan-to-value on a conventional mortgage exceeds 80 per cent, the bank has the right to direct the borrower to bring it under that 80 per cent threshold or to obtain an appraisal proving the fair market value is indeed higher. The new wording replaces a similar clause that sets that trigger at 75 per cent but limits the scenario to instances where interest rate fluctuations have driven LTV over that 75 per cent mark.

Mulhern believes that new, wider clause speaks to the lender’s concerns about a possible market correction and its power to drive down property values.

“In the new clause, it states that if at any time the principal balance exceeds the max LTV.” he said. “This protects the lender in case of property devaluation. “

But does the move from 75 per cent to 80 per cent cancel out any potential negative exposure for the client? Mulhern isn’t so sure.

“Something that is outside the borrower’s control, property values, can cause them to have to come up with a significant amount of money or the mortgage will be called,” he explained.

The amendment took place sometime last year, according to Mulhern, and he was only made aware of it because of an increase in variable rate mortgages he recently arranged.

“Unless I’m reading it incorrectly this type of clause has nothing to do with rate fluctuations and everything to do with loan-to-value,” Mulhern said. “Property value decreases would have a huge impact on all TD variable rate mortgages.”

The clauses are compared side-by-side below.

Old:

New:

“I went to the BDM and I ran it past them and asked if I was reading it wrong or not understanding it properly and they said the intention is as it states,” Patrick Mulhern of Invis Mulhern Mortgages told MortgageBrokerNews.ca. “They didn’t explain why the change was made.”

He suspects that change is really a hedge against any future price correction for Canadian real estate.

Under the terms of the new clause, if, at any time and for any reason, the loan-to-value on a conventional mortgage exceeds 80 per cent, the bank has the right to direct the borrower to bring it under that 80 per cent threshold or to obtain an appraisal proving the fair market value is indeed higher. The new wording replaces a similar clause that sets that trigger at 75 per cent but limits the scenario to instances where interest rate fluctuations have driven LTV over that 75 per cent mark.

Mulhern believes that new, wider clause speaks to the lender’s concerns about a possible market correction and its power to drive down property values.

“In the new clause, it states that if at any time the principal balance exceeds the max LTV.” he said. “This protects the lender in case of property devaluation. “

But does the move from 75 per cent to 80 per cent cancel out any potential negative exposure for the client? Mulhern isn’t so sure.

“Something that is outside the borrower’s control, property values, can cause them to have to come up with a significant amount of money or the mortgage will be called,” he explained.

The amendment took place sometime last year, according to Mulhern, and he was only made aware of it because of an increase in variable rate mortgages he recently arranged.

“Unless I’m reading it incorrectly this type of clause has nothing to do with rate fluctuations and everything to do with loan-to-value,” Mulhern said. “Property value decreases would have a huge impact on all TD variable rate mortgages.”

The clauses are compared side-by-side below.

Old:

New: