BEACON 9 has caused quite a stir among brokers, with many arguing the positives and negatives

BEACON 9 has caused quite a stir among brokers, with many arguing the positives and negatives.

Change is inevitable, and when it impacts broker business you know industry players will have an opinion. Equifax recently announced its new BEACON score and brokers have had varying opinions about the success of the change.

“We are going to start to see some very bad effects of BEACON 9; today we had a client change their mind about the product they wanted, we had to go to a new lender and run a new bureau because the old CB was 40 days old,” Ron Butler, a broker with Butler Mortgage, wrote in the comments section of MortgageBrokerNews.ca. “Old Score: 742, New Score: 648. The only changes: balances on the only two trade lines the client had increased closer to the credit limit by $200 each. No other change.”

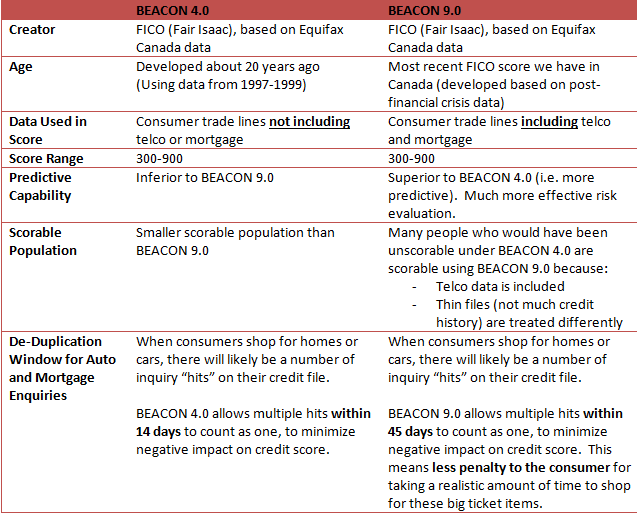

BEACON 9 is “the newest FICO Score version in Canada to help you make credit decisions with confidence,” according to the user guide provided to brokers, which was obtained by MortgageBrokerNews.ca. “It allows you to effectively evaluate new prospects by predicting the probability of an account going ‘bad’.

Some brokers have noticed an uptick in BEACON scores, with one noting a record-breaking score coming in.

“Clients who pay their mortgages on time, that will be reflected on the credit score. Yesterday, one of my underwriters saw a 900 BEACON, which I always thought was a myth, the unicorn, the White Whale,” Mike Havery, a mortgage planner with Mortgage Architects, recently told MortgageBrokerNews.ca.

However, the negative impacts will outweigh the positives, according to Butler.

“I think we should all realize once a score goes past 760 no one cares, the insurers, the lenders and the background investors do not care,” he wrote. “But if a score goes below 700 or 680 it may be a very big deal to mortgage brokers; it may lose access to certain rates under 700 and under 680 totally changes the debt ratio calculations.”

Some have claimed BEACON 9 places more emphasis on credit utilization, which has made for lower scores coming in. However, Equifax denies this.

“BEACON 9 does not place any higher weight on credit utilization than previous versions of the score,” Tom Carroll, director of communications at Equifax Canada wrote in an email to MortgageBrokerNews.ca. Carroll also provided a fact sheet on the new score.

Change is inevitable, and when it impacts broker business you know industry players will have an opinion. Equifax recently announced its new BEACON score and brokers have had varying opinions about the success of the change.

“We are going to start to see some very bad effects of BEACON 9; today we had a client change their mind about the product they wanted, we had to go to a new lender and run a new bureau because the old CB was 40 days old,” Ron Butler, a broker with Butler Mortgage, wrote in the comments section of MortgageBrokerNews.ca. “Old Score: 742, New Score: 648. The only changes: balances on the only two trade lines the client had increased closer to the credit limit by $200 each. No other change.”

BEACON 9 is “the newest FICO Score version in Canada to help you make credit decisions with confidence,” according to the user guide provided to brokers, which was obtained by MortgageBrokerNews.ca. “It allows you to effectively evaluate new prospects by predicting the probability of an account going ‘bad’.

Some brokers have noticed an uptick in BEACON scores, with one noting a record-breaking score coming in.

“Clients who pay their mortgages on time, that will be reflected on the credit score. Yesterday, one of my underwriters saw a 900 BEACON, which I always thought was a myth, the unicorn, the White Whale,” Mike Havery, a mortgage planner with Mortgage Architects, recently told MortgageBrokerNews.ca.

However, the negative impacts will outweigh the positives, according to Butler.

“I think we should all realize once a score goes past 760 no one cares, the insurers, the lenders and the background investors do not care,” he wrote. “But if a score goes below 700 or 680 it may be a very big deal to mortgage brokers; it may lose access to certain rates under 700 and under 680 totally changes the debt ratio calculations.”

Some have claimed BEACON 9 places more emphasis on credit utilization, which has made for lower scores coming in. However, Equifax denies this.

“BEACON 9 does not place any higher weight on credit utilization than previous versions of the score,” Tom Carroll, director of communications at Equifax Canada wrote in an email to MortgageBrokerNews.ca. Carroll also provided a fact sheet on the new score.